Join Steve LaFrance, CFP® with Blakely Financial as he updates you on the last month in 3 minutes.

Blakely Financial

![]()

Join Steve LaFrance, CFP® with Blakely Financial as he updates you on the last month in 3 minutes.

There’s good news for older Americans at high-risk of developing dementia: simple steps to stay mentally and physically active improved thinking and helped keep Alzheimer’s disease at bay. And it didn’t take long.

Lifestyle changes including exercise, a better diet, and more mental and social activity yielded significant protection within two years, according to a large clinical trial published Monday. To qualify for the study, participants had to have various risk factors for brain decline, like consuming a poor diet and not exercising regularly. Others had a gene mutation tied to Alzheimer’s disease.

While brain function starts to worsen in a person’s sixties, the results indicate that switching up one’s routine even later in life can stall the onset of dementia. Making such changes appeared to slow the cognitive aging clock by one to two years, said Laura Baker, a professor of internal medicine at Wake Forest University of Medicine and one of the study leaders.

The key takeaways are to “move more, sit less, add color to your plate, learn something new, and stay connected,” Baker said at the Alzheimer’s Association International Conference in Toronto, where the results were presented. “Challenge yourself to do this on a regular basis.”

The findings were simultaneously published in the Journal of the American Medical Association.

The U.S. Study to Protect Brain Health Through Lifestyle Intervention to Reduce Risk, known as Pointer, is the largest lifestyle intervention trial for Alzheimer’s disease completed in the U.S. It included more than 2,000 adults between the ages of 60 and 79 in structured and self-guided intervention groups.

Cognitive function improved in both, but those getting structured support had a significantly greater benefit than those in the self-guided group.

The program recommended cardiovascular exercise for 30 minutes, four days a week, and a low-salt diet with a focus on brain-healthy foods like dark leafy greens, berries, whole grains and coldwater fish. Participants in the structured group completed “brain training” computer games three times a week.

The structured group had 38 meetings with their peers over the two-year study to set goals and keep others accountable. The self-guided group met much less often — six times over the two years — but received the same information.

The POINTER trial replicated the 2015 landmark FINGER study, or Finnish Geriatric Intervention Study to Prevent Cognitive Impairment, to assess whether those findings applied to the larger and often less healthy US population.

This article was provided by Bloomberg News.

Join Steve LaFrance, CFP®, AIF®, ChSNC®, MBA, as he explains what you need to know about the “Big Beautiful Bill,” what it is, and how it could impact your financial future. All in just 3 minutes.

Join Steve LaFrance, CFP® with Blakely Financial as he updates you on the last month in 3 minutes.

Join Steve LaFrance, CFP® with Blakely Financial as he updates you on the last month in 3 minutes.

From Robert Blakely, Founder of Blakely Financial:

“It is exciting to be celebrating 30 years in the financial planning and investment management field. I started in 1995 with no clients and just the desire to help make a difference in people’s lives through financial planning. As with any new business the first few years were tough. In 2000 I decided to partner with Commonwealth Financial Network which was an important decision for myself and our clients. With the network of Commonwealth advisors I was able to leverage years of experience of others and our growth truly began. I added my first employee in 2001 and another experienced advisor joined in 2002. My wife, Donna, who had been there with her support for years, joined us in 2003.

We can truly state that we have been blessed in ways that I never really imagined when I first started. We have been blessed with amazing friendships and meaningful relationships for which we will be forever grateful.

As excited and optimistic as I was when I started in 1995, today in 2025, I am as equally so for the future of our firm and our clients. We have great and caring team members. and with Emily Promise as President and Owner of Blakely Financial I truly believe the future for our clients and team is going to be even better.

Thank you to everyone for your friendship, trust, confidence and support for the past 30 years.”

Since its founding, Blakely Financial has prioritized individualized financial strategies tailored to each client’s unique goals and needs. We believe in building lasting relationships and guiding clients through every stage of life, from wealth accumulation to retirement and succession planning.

This client-first approach has earned national recognition, including Blakely Financial’s recent honor as one of Forbes’ Best-in-State Wealth Management Teams. The firm’s success reflects the deep trust our clients place in us, and the firm remains committed to delivering financial strategies to support their present and future.

Over the past three decades, Blakely Financial has evolved, expanding our specialization and team to better serve our clients. Some of our key milestones include:

At Blakely Financial, we know financial planning is about more than investments. We work to build trust and guide individuals and families through life’s milestones to secure their financial futures. Our clients turn to us for:

The firm’s commitment to acting as a fiduciary ensures that every recommendation is made with our client’s best interests in mind.

Emily Promise, now leading Blakely Financial, is committed to continuing the firm’s legacy while embracing new opportunities for growth and innovation. With our team of experienced advisors, the firm is well-positioned to support clients through comprehensive financial planning, estate strategies, and long-term investment solutions.

Blakely Financial remains dedicated to our community-focused approach, ensuring clients feel supported, empowered, and confident in their financial futures.

Blakely Financial’s success over the past 30 years is a testament to the loyalty and trust of our clients. We are honored to be a part of their financial journeys and are committed to helping families, individuals, and business owners achieve their financial goals for generations to come.

As we celebrate this milestone, we look forward to the next 30 years of growth, innovation, and continued service as a trusted financial partner to our clients and community. To learn more about our services and how we can support your financial goals, contact the Blakely Financial team today.

Join Steve LaFrance, CFP® with Blakely Financial as he updates you on the last 3 months in 3 minutes.

Donna Blakely recently volunteered with the Junior League of High Point and helped teach a Crock-Pot cooking class at the YWCA to young moms. It was an educational workshop that included healthy eating focused on the nutritional needs of women and children. The JLHP provided each participant with a crock-pot, recipe book, and ingredients to help these moms recreate the meal at home that was demonstrated to them during the class. Anytime there is food and cooking involved, Donna loves to help out!

Presented by Robert Blakely, Emily Promise, and Steve LaFrance

The next phase in the Russia-Ukraine crisis has begun, as Russia has launched attacks on Ukraine. With a war underway, it’s unsurprising that the markets are reacting. Before the market opened on Thursday, U.S. stock futures were down between 2 1/2 percent and 3 1/2 percent, while gold was up by roughly the same amount. In addition, the yield on 10-Year U.S. Treasury securities has dropped sharply. International markets were down even more than the U.S. markets, as investors fled to the more comfortable haven of U.S. securities.

News of the invasion is hitting the markets hard right now, but the real question is whether that hit will last. It probably will not. History shows the effects are likely to be limited over time. In retrospect, this event is not the only time we have seen military action in recent years. And it’s not the only time we’ve seen aggression from Russia. In none of these cases were the effects long-lasting.

Let’s look back at the Russian invasion of Georgia and the Russian takeover of Crimea, which is part of Ukraine. In August 2008, Russia invaded the Republic of Georgia. The U.S. markets dropped by about 5 percent, then rebounded to end the month even. Then, in February and March 2014, Russia invaded and annexed Crimea. Again, the U.S. markets dropped about 6 percent on the invasion but rallied to end March higher. In both of these cases, the initial market drops were erased quickly.

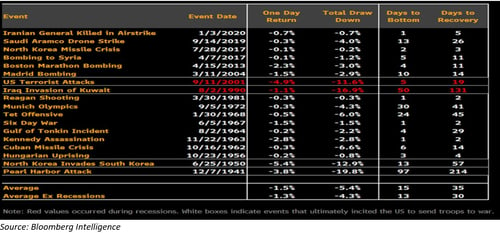

We essentially see the same pattern when looking at a broader range of events. For example, the chart below shows market reactions to other acts of war, both with and without U.S. involvement. Historically, the data shows a short-term pullback—as we will likely see today—followed by a bottom within the next couple of weeks. Exceptions include the 9/11 terrorist attacks, the Iraqi invasion of Kuwait, and, looking further back, the Korean War and Pearl Harbor attacks.

Still, even with these exceptions, the market reaction was limited both on the day of the event and during the overall time to recovery. Moreover, comparing the data provides valuable context for recent events. For example, as tragic as the invasion of Ukraine is, its overall effect will likely be much closer to that of the Russian invasion of Ukraine in 2014, in which Russia annexed Crimea than it will be to the aftermath of 9/11.

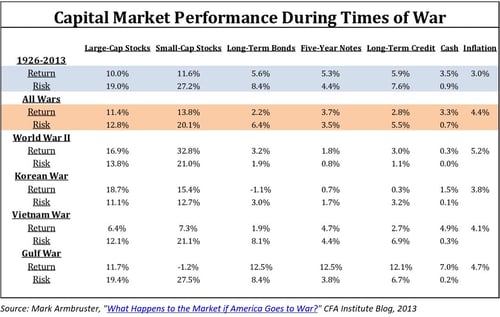

But even with the short-term effects discounted, should we fear that somehow the war or its impact will derail the economy and markets? Here, too, the historical evidence is encouraging, as demonstrated by the chart below. Returns during wartime have historically been better than all returns, not worse. Although the war in Afghanistan is not included in the chart, it too matches the pattern. During the first six months of that war, the Dow gained 13 percent, and the S&P 500 gained 5.6 percent.

Sources: The indices used for each asset class are as follows: the S&P 500 Index for large-Cap stocks; CRSP Deciles 6-10 for small-cap stocks; long-term U.S. government bonds for long-term bonds; five-year U.S. Treasury notes for five-year notes; long-term U.S. corporate bonds for long-term credit; one-month Treasury bills for cash; and the Consumer Price Index for inflation. All index returns are total returns for that index.

Returns for a wartime period are calculated as the index’s returns four months before the war and during the entire war itself. Returns for “All Wars” are the annualized geometric return of the index over all “wartime periods.” Risk is the annualized standard deviation of the index over the given period. Past performance is not indicative of future results.

This data is not presented to say that the Russia-Ukraine crisis won’t bring real effects and hardship. Oil prices are up to levels not seen since 2014, which was the last time Russia invaded Ukraine. Higher oil and energy prices will hurt economic growth and drive inflation worldwide, especially in Europe and the U.S. This environment will be a headwind as we advance.

Will we see effects from the headwind caused by the Ukraine invasion? Very likely. Will they derail the economy? Not likely at all. During recent waves of Covid-19, the U.S. economy demonstrated substantial momentum, which should move us through the current headwind until markets normalize. Moreover, as has happened before, we already see U.S. production increase, which should help bring prices back down.

The Ukraine invasion has created current market turbulence; we should look at what history tells us. First, past conflicts have not derailed either the economy or the markets over time. Historically, the U.S. has survived and even thrived during wars.

Although the current events with the Russia-Ukraine crisis have unique elements, they’re more of what we’ve seen in the past. Events like yesterday’s invasion do come along regularly. Part of successful investing—sometimes the most challenging—is not overreacting. If you’re comfortable with the risks you’re taking, you might not be making any changes—except perhaps to start looking for some stock bargains. Consider whether your portfolio allocations are at a comfortable risk level if you’re worried. If they’re not, talk to your advisor.

This material is intended for informational/educational purposes only. It should not be construed as investment advice, a solicitation, or a recommendation to buy or sell any security or investment product. Certain sections of this commentary contain forward-looking statements that are based on our reasonable expectations, estimates, projections, and assumptions. Forward-looking statements are not guarantees of future performance and involve certain risks and uncertainties, which are difficult to predict. All indices are unmanaged and are not available for direct investment by the public. Past performance is not indicative of future results. The S&P 500 is based on the average performance of the 500 industrial stocks monitored by Standard & Poor’s. The Dow Jones Industrial Average (‘the Dow’) is a price-weighted measurement stock market index of 30 prominent companies listed on stock exchanges in the United States.

Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other expert advice we can provide towards your financial well-being.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals.

Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser.

Diversification and asset allocation programs do not assure a profit or protect against loss in declining markets, and cannot guarantee that any objective or goal will be achieved.

Authored by Brad McMillan, CFA®, CAIA, MAI, managing principal, chief investment officer, at Commonwealth Financial Network®.

© 2022 Commonwealth Financial Network®

You’ve been doing the right thing financially for many years, saving for your child’s education and your retirement. Yet now, as both goals loom in the years ahead, you may wonder what else you can do to help your child (or children) receive a quality education without compromising your own retirement goals.

Start by reviewing the financial aid process and understanding how financial need is calculated. Colleges and the federal government use different formulas to determine need by looking at a family’s income (the most crucial factor), assets, and other household information.

A few key points:

Financial aid takes two forms: need-based aid and merit-based aid. Although middle- and higher-income families typically have a more challenging time receiving need-based aid, there are some ways to reposition your finances to potentially enhance eligibility:

Many colleges use merit-aid packages to attract students, regardless of financial need. As your family explores colleges in the years ahead, be sure to investigate merit-aid opportunities as well. A net price calculator, available on every college website, can give you an estimate of how much financial aid (merit- and need-based) your child might receive at a particular college.

What if you’ve done all you can and still face a sizable gap between how much college will cost and how much you have saved? To help your child graduate with as little debt as possible, you might consider borrowing or withdrawing funds from your retirement savings. Though tempting, this is not an ideal move. While your child can borrow to finance their education, you generally cannot take a loan to fund your retirement. If you make retirement savings and debt reduction (including a mortgage) a priority now, you may be better positioned to help your child repay any loans later.

Some Parents Use Retirement Funds to Pay for College

Source: Sallie Mae, 2021

Consider speaking with a financial professional about how these strategies may help you balance these two challenging and important goals. Of course, there is no assurance that working with a financial professional will improve investment results.

Withdrawals from traditional IRAs and most employer-sponsored retirement plans are taxed as ordinary income. They may be subject to a 10% penalty tax if taken before age 59½ unless an exception applies. (IRA withdrawals used for qualified higher-education purposes avoid the early-withdrawal penalty.)

1) College Savings Plan Network, 2021