Blakely Financial

![]()

If you have ever been caught off-guard by a large medical bill, a long-running practice known as balance billing might be the reason. A balance bill — which is the difference between an out-of-network provider’s normal charges for a service and a lower rate reimbursed by insurance — can amount to thousands of dollars.

Many consumers are already aware that it usually costs less to seek care from in-network health providers, but that’s not always possible in an emergency. Complicating matters, some hospitals and urgent-care facilities rely on physicians, ambulances, and laboratories that are not in the same network. In fact, a recent survey found that 18% of emergency room visits resulted in at least one surprise bill.1

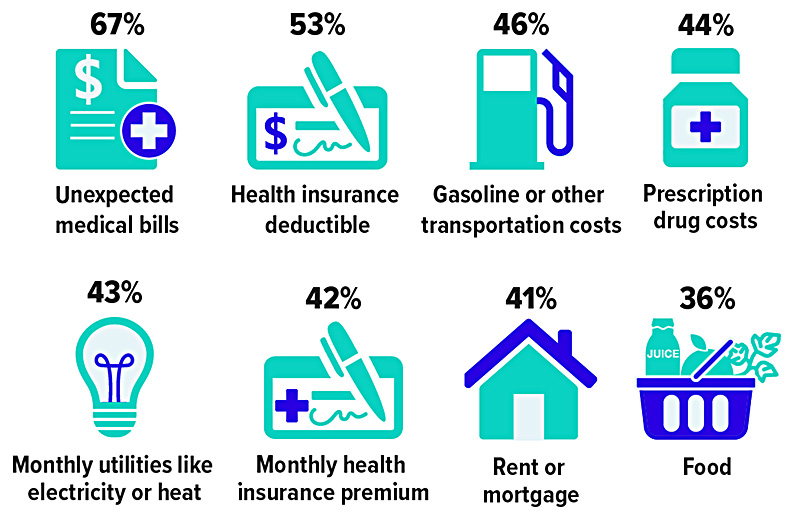

Who’s Afraid of High Health-Care Costs? Most People

Percent of surveyed adults who say they are worried about being able to afford the following expenses

Source: Kaiser Family Foundation and JAMA, 2020

The No Surprises Act was included in the omnibus spending bill enacted by the federal government at the end of 2020. The new rules will help ensure that consumers do not receive unexpected bills from out-of-network providers they didn’t choose or had no control over. For example, once the new law takes effect in 2022, patients will not receive balance bills for emergency care or non-emergency care at in-network hospitals when out-of-network providers unknowingly treat them. (A few states already have laws that prevent balance billing unless the patient agrees to costlier out-of-network care ahead of time.)

Patients will be responsible only for the deductibles and copayment amounts they would owe under the in-network terms of their insurance plans. Instead of charging patients, health providers will negotiate a fair price with insurers (and settle disputes with arbitration). This change applies to doctors, hospitals, and air ambulances — but not ground ambulances.

Some patients purposely seek care from out-of-network health providers, such as a trusted family physician or a highly regarded specialist, when they believe the quality of care is worth the extra cost. In these non-emergency situations, physicians can still balance-bill their patients. However, a good-faith cost estimate must be provided, and a consent form must be signed by the patient at least 72 hours before treatment. In addition, some providers are barred from seeking consent to balance-bill for their services, including anesthesiologists, radiologists, pathologists, neonatologists, assistant surgeons, and laboratories.

The fact that millions of consumers could be saved from surprise medical bills is something to celebrate. Still, many people may struggle to cover their out-of-pocket health expenses, in some cases because they are uninsured or simply due to high plan deductibles or rising costs in general. Covered workers enrolled in family coverage contributed $5,588, on average, toward the cost of premiums in 2020, with deductibles ranging from $2,700 to more than $4,500, depending on the type of plan.2

When arranging non-emergency surgery or other costly treatment, you may want to take your time choosing a doctor and a facility because charges can vary widely. Don’t hesitate to ask for detailed estimates and try to negotiate a better price.

If you receive a higher-than-expected bill, don’t assume it is set in stone. Check hospital bills closely for errors, check billing codes, and dispute charges that you think insurance should cover. If all else fails, offer to settle your account at a discount.

1-2) Kaiser Family Foundation, 2020

Unless you complete your holiday shopping before Halloween, you might be enticed by Black Friday and Cyber Monday deals. These tips may help you save time and money.

Create a budget. Before you start shopping, establish an overall budget. Make a list of gifts you will need to buy and decide exactly how much you can afford to spend on each person.

Beat the crowds. If you shop early in the season, items are more likely to be in stock and you may face fewer shipping delays. Sales often start well before Black Friday, so keep an eye out for special promotions at least a week or two ahead. Signing up for online or social media deal alerts can help.

Research pricing. Knowing whether a deal is truly good can be tricky, but many websites and phone apps are available that can help you compare items and prices as you shop.

Set up accounts. To complete purchases quickly, consider saving your information and shipping addresses on trusted online accounts with your favorite retailers. Make it a habit to search for promotional and coupon codes that you can use at checkout. Review shipping costs, too, to avoid paying more than you expect.

Track purchases. To help you stick with your budget, keep track of what you spend. If you’re shopping with credit, try using one card for everything so you can quickly review your spending. A rewards card may give you cash back, points, or miles that you can redeem in the future, but watch out for high-interest rates if you can’t pay off the balance in full.

Use cash.Consider using a debit card or cash for in-store purchases. Carrying only a predetermined amount of money in your wallet may help you avoid overspending.

Pay attention to the fine print.Retailers may have special policies in place for the holiday season. Knowing the time limits for exchanges or returns is especially important when you’re shopping early. Ask for gift receipts and keep your own copies.

Watch out for exclusions.Promotional prices might be limited to certain items and may expire quickly, so understand the details.

Look for price guarantees.If you buy an item that later goes on sale, some retailers will refund the difference within certain time limits. Retailers may also match a competitor’s price on an identical item (you may need to provide proof of the purchase).

Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals.

Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser.

As we approach year-end, now is a great time to take advantage of several end-of-the-year financial planning tips that you may have been procrastinating on. Watch now for tips from Robert Blakely, Certified Financial Planner®!

The risks we saw in September are real, but there are signs those risks may be fading—and that the very real positive trends from July and August will reassert themselves. Watch our latest video for more insights into how the markets have performed in the last quarter.

Whether you’ve been saving and planning for your child’s college education for the past 18 years or you just recently started discussing college plans with your child, senior year is the time when many decisions need to be made.

The summer before your child’s senior year is a good time to narrow down college choices. If you haven’t done so already, now is the time to research colleges online, request catalogs, attend college fairs, and visit campuses to help finalize the list of schools.

Be sure to note specific school deadlines for applications, scholarships, and financial aid forms and check them regularly. The following calendar is a general overview of the application and financial aid process.

| Fall | Winter | Spring | Summer |

| Research colleges online, attend college fairs, and visit college campuses to make a final list | General admission applications are typically due in December or January—confirm the deadline for each school | Review financial aid packages offered by various colleges; compare out-of-pocket costs at each college | Buy school and dorm supplies |

| Early decision/early action applications are typically due in October or November—confirm the deadline for each school | Submit college PROFILE financial aid form and college-specific financial aid forms where necessary | Review ongoing requirements of any college scholarships if selected | Work to earn spending money |

| Attend financial aid night at local high school | Confirm that colleges have received all application and financial aid materials | Make a final decision and notify the college by May 1 | Prepare to move if you are going away to school |

| The federal government’s financial aid application, the FAFSA, can be filed as early as October 1 | Continue to apply for college scholarships | Pay required college deposit | Sign student loan promissory note and receive federal student loan counseling if applicable |

| Apply for college-specific scholarships | Research and apply for private scholarships | Sign up for college orientation session if required | Off to college! |

| An independent third party has developed this resource.

Commonwealth Financial Network is not responsible for their content and does not guarantee their accuracy or completeness, and they should not be relied upon as such. These materials are general in nature and do not address your specific situation. For your specific investment needs, please discuss your individual circumstances with your representative. Commonwealth does not provide tax or legal advice, and nothing in the accompanying pages should be construed as specific tax or legal advice. Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through Blakely Financial or CES Insurance Agency

This communication is strictly intended for individuals residing in the state(s) of AK, AZ, AR, CA, CO, FL, GA, IL, IA, MA, MD, MI, MN, MS, MO, NJ, NY, NC, OK, PA, SC, SD, TN, TX, VA, WV, and WI. No offers may be made or accepted from any resident outside the specific states referenced. |

|

| Prepared by Broadridge Advisor Solutions Copyright 2021. |

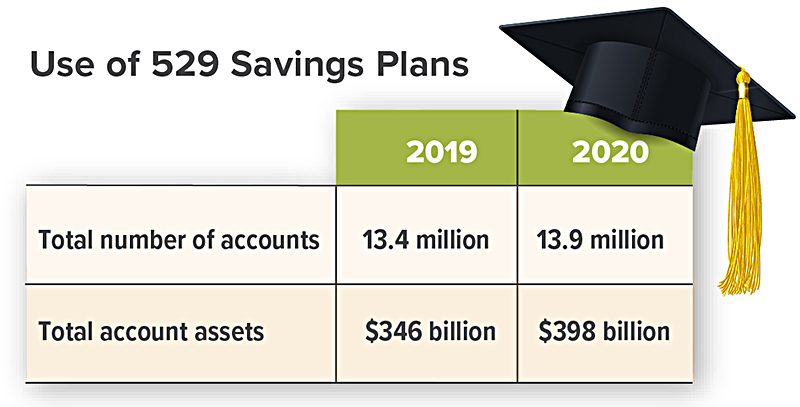

529 plans are a favored way to save for college due to the tax benefits and other advantages they offer when funds are used to pay a beneficiary’s qualified college expenses. However, up until now, the FAFSA (Free Application for Federal Student Aid) treated grandparent-owned 529 plans more harshly than parent-owned 529 plans. This will change thanks to the FAFSA Simplification Act that was enacted in December 2020. The new law streamlines the FAFSA and changes the formula used to calculate financial aid eligibility.

Under current rules, parent-owned 529 plans are listed on the FAFSA as a parent asset. Parent assets are counted at a rate of 5.64%, which means 5.64% of the value of the 529 account is deemed available to pay for college. Later, when distributions are made to pay college expenses, the funds aren’t counted; the FAFSA ignores distributions from a parent 529 plan.

By contrast, grandparent-owned 529 plans do not need to be listed as an asset on the FAFSA. This sounds like a benefit. However, the catch is that any withdrawals from a grandparent-owned 529 plan are counted as untaxed student income and assessed at 50% in the following year. This can have a negative impact on federal financial aid eligibility.

Example: Ben is the beneficiary of two 529 plans: a parent-owned 529 plan with a value of $25,000 and a grandparent-owned 529 plan worth $50,000. In Year 1, Ben’s parents file the FAFSA. They must list their 529 account as a parent asset but do not need to list the grandparent 529 account. The FAFSA formula counts $1,410 of the parent 529 account as available for college costs ($25,000 x 5.64%). Ben’s parents then withdraw $10,000 from their account, and Ben’s grandparents withdraw $10,000 from their account to pay college costs in Year 1.

In Year 2, Ben’s parents file a renewal FAFSA. Again, they must list their 529 account as a parent asset. Let’s assume the value is now $15,000, so the formula will count $846 as available for college costs ($15,000 x 5.64%). In addition, Ben’s parents must also list the $10,000 distribution from the grandparent 529 account as untaxed student income, and the formula will count $5,000 as available for college costs ($10,000 x 50%). In general, the higher Ben’s available resources, the less financial need he is deemed to have.

Under the new FAFSA rules, grandparent-owned 529 plans still do not need to be listed as an asset, and distributions will no longer be counted as untaxed student income. In addition, the new FAFSA will no longer include a question asking about cash gifts from grandparents. This means that grandparents will be able to help with their grandchild’s college expenses (either with a 529 plan or with other funds) with no negative implications for federal financial aid.

However, there’s a caveat: Grandparent-owned 529 plans and cash gifts will likely continue to be counted by the CSS Profile, an additional aid form typically used by private colleges when distributing their own institutional aid. Even then, it’s not one-size-fits-all — individual colleges can personalize the CSS Profile with their own questions, so the way they treat grandparent 529 plans can differ.

The new, simplified FAFSA opens on October 1, 2022, and will take effect for the 2023-2024 school year. However, grandparents can start taking advantage of the new 529 plan rules in 2021. That’s because 2021 is the “base year” for income purposes for the 2023-2024 FAFSA, and under the new FAFSA, a student’s income will consist only of data reported on the student’s federal income tax return. Because any distributions taken in 2021 from a grandparent 529 account won’t be reported on the student’s 2021 tax return, they won’t need to be reported as student income on the 2023-2024 FAFSA.

Consider the investment objectives, risks, charges, and expenses associated with 529 plans before investing. This information and more is available in the plan’s official statement and applicable prospectuses, including details about investment options, underlying investments, and the investment company; read it carefully before investing. Also, consider whether your state offers a 529 plan that provides residents with favorable state tax benefits and other benefits, such as financial aid, scholarship funds, and protection from creditors. As with other investments, there are generally fees and expenses associated with participation in a 529 plan. There is also the risk that the investments may lose money or not perform well enough to cover college costs as anticipated. In addition, for withdrawals not used for higher-education expenses, earnings may be subject to taxation as ordinary income and a 10% federal income tax penalty.

Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other specialized advice we can provide towards your financial well-being.

BLAKELY FINANCIAL, INC. is located at 1022 Hutton Ln., Suite 109, High Point, NC 27262, and can be reached at (336) 885-2530.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals.

| Commonwealth Financial Network is not responsible for their content and does not guarantee their accuracy or completeness, and they should not be relied upon as such. These materials are general in nature and do not address your specific situation. For your specific investment needs, please discuss your individual circumstances with your representative. Commonwealth does not provide tax or legal advice, and nothing in the accompanying pages should be construed as specific tax or legal advice. Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser. Fixed insurance products and services offered through Blakely Financial or CES Insurance Agency

This communication is strictly intended for individuals residing in the state(s) of AK, AZ, AR, CA, CO, FL, GA, IL, IA, MD, MI, MN, MS, MO, NJ, NY, NC, OK, PA, SC, SD, TN, TX, VA, WV, and WI. No offers may be made or accepted from any resident outside the specific states referenced. |

|

| Prepared by Broadridge Advisor Solutions Copyright 2021. |

In March 2021, the widening availability of COVID-19 vaccinations, signs of improving economic conditions, and a third, $1.9 trillion stimulus package brought about more optimistic growth projections. Even though a healthy economy could be good news for many businesses and the financial markets, rising inflation expectations caused a multi-week sell-off in U.S. government bonds that pushed up longer-term yields and sent the Nasdaq Composite Index into correction territory on March 8, 2021.1

Promising a patient approach, the Federal Reserve stated that it would not raise interest rates until the labor market fully recovers and inflation moderately exceeds the 2% target for some time.2 But some investors worry that sharply higher inflation could force policymakers to boost rates sooner than originally expected.

Here’s a closer look at some specific types of investment risk that could influence individual stock prices and/or cause broader market swings during the second half of 2021.

Inflation and interest rates are two different but closely related investment risks. The Federal Reserve is tasked with fostering full employment and controlling inflation. One way it balances these two goals is by lowering interest rates to stimulate business activity or raising rates to help slow inflation when the economy is heating up too fast.

High inflation erodes the value of investment returns, but when interest rates rise, bond values fall (and vice versa). These risks are obvious considerations for bond owners, but they also impact stocks. When goods, services, and credit cost more, consumers have less purchasing power, which can hurt company earnings and stock prices as well.

Rising bond yields might continue to have a negative effect on stock values, because as they move up, borrowing costs for most businesses also rise, cutting into profits. Higher yields could also entice risk-averse investors to sell their stocks and buy more stable bonds instead.

Some government actions (such as antitrust lawsuits, higher taxes, and more stringent regulations or standards) make it more difficult and expensive for companies to do business, which can adversely affect their earnings and stock prices. On the other hand, government subsidies and tariffs on foreign products can provide competitive advantages.

The Justice Department, Federal Trade Commission, and numerous states are in the midst of antitrust lawsuits or major investigations into the business practices of several market-dominating tech companies.3 In another example, the Securities and Exchange Commission is considering new standards for corporate disclosures related to environmental, social, and governance risks.4

Headline risk refers to the possibility that events reported in the media could hurt a company’s reputation and/or earnings prospects. Troubling news can cause market backlash against a specific company or an entire industry. Companies try to manage this risk through public relations campaigns and other efforts to generate positive news that leaves a good impression on consumers. Events that threaten to disrupt business activity nationwide, regionally, or around the world can cause sudden stock market declines.

The market responds to news, good or bad, almost every day. For this reason, your portfolio should be designed to weather a range of market conditions and have a risk profile that reflects your ability to endure periods of market volatility, both financially and emotionally.

The principal value of bonds may fluctuate with changes in interest rates and market conditions. Bonds redeemed prior to maturity may be worth more or less than their original cost. The return and principal value of stocks fluctuate with changes in market conditions. Shares, when sold, may be worth more or less than their original cost. Investments seeking to achieve higher yields also involve a higher degree of risk.

BLAKELY FINANCIAL, INC. is located at 1022 Hutton Ln., Suite 109, High Point, NC 27262, and can be reached at (336) 885-2530.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals.

Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser

Presented by Robert C. Blakely

Most people carry some debt, whether a student loan, a mortgage, or a car loan. Indeed, making large purchases using someone else’s money is often a smart financial move. Borrowing is convenient, allowing you to purchase big-ticket items with less out-of-pocket cash. And, with today’s attractive interest rates, it’s a relatively low cost. But taking on any amount of debt comes with risk. A financial setback can reduce your ability to repay a loan, and any amount of debt may prevent you from taking advantage of other financial opportunities.

When analyzing your ability to carry debt, take a close look at your personal finances, focusing on the following factors:

Liquidity. If you suddenly lost your job, would you have enough cash at the ready to cover your current liabilities? It’s a good idea to maintain an emergency fund to cover three to six months’ worth of expenses. But don’t go overboard. Guard against keeping more than 120 percent of your six-month expense estimate in low-yielding investments. And don’t let more than 5 percent of your cash reserves sit in a non-interest-bearing checking account.

Current debt. Your total contractual monthly debt payments (i.e., the minimum required payments) should come to no more than 36 percent of your monthly gross income. In addition, the amount of consumer debt you carry—credit card balances, automobile loans, leases, and debt related to other lifestyle purchases—should amount to less than 10 percent of your monthly gross income. If your consumer debt ratio is 20 percent or more, avoid taking on additional debt.

Housing expenses. As a general rule, your monthly housing costs—including your mortgage or rent, home insurance, real estate taxes, association fees, and other required expenses—shouldn’t amount to more than 31 percent of your monthly gross income. However, if you’re shopping for a mortgage, consider that lenders use their own formulas to calculate how much home you can afford based on your gross monthly income, current housing expenses, and other long-term debt, such as auto and student loans. For example, for a mortgage insured by the Federal Housing Administration, your housing expenses and long-term debt should not exceed 43 percent of your monthly gross income.

Savings. Although the standard recommended savings rate is 10 percent of gross income, your guideline should depend on your age, goals, and stage of life. For example, you should save more as you age, and as retirement nears, you may need to ramp up your savings to 20 percent or 30 percent of your income. Direct deposits, automatic contributions to retirement accounts, and electronic transfers from checking accounts to savings accounts can help you make saving a habit.

If you’re in the market for a new home, the myriad of mortgage choices can be overwhelming. Fixed or variable interest rate? Fifteen- or thirty-year term? If it were merely a question of which mortgage provided the lowest long-term costs, the answer would be simple. But, in reality, the best mortgage for a particular household depends on how long the homeowner plans to stay in the house, the available down payment, the predictability of cash flow, and the borrower’s tolerance for fluctuating payments.

How long will you be there? One rule of thumb is to choose a mortgage based on how long you plan to stay in the home. If you plan to stay 5 years or less, consider renting. If you plan to live in the house for 5 to 10 years and have a high tolerance for fluctuating payments, consider a variable-rate mortgage for a longer-term, such as 30 years, to help keep the cost down. If the home is a long-term investment, choose a fixed-rate mortgage with a shorter term, such as 15 or 20 years.

Is a variable-rate mortgage worth the risk? Because the monthly payments are typically lower with variable-rate mortgages, they are generally the easiest to qualify for—and may enable you to purchase a more expensive home.

Variable-rate mortgages also allow you to take advantage of falling interest rates without the cost of refinancing. But keep in mind that it’s generally not wise to take on a variable-rate mortgage simply because you qualify for one. Although these mortgages offer the lowest interest rate, they’re also the riskiest, as the monthly payment can increase to an amount that may prove difficult to meet. Again, selecting a shorter loan term, such as 15 years, can help lessen this risk.

Remember, when it comes to taking on debt, the loan amount you qualify for and the amount you can comfortably afford to repay may not be the same. So be sure to consider your special circumstances before taking on debt to buy a home or make another major purchase. For more tips on homeownership, please read our article on Five Tips When Shopping for a Mortgage.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to ensure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other expert advice we can provide towards your financial well-being.

ROBERT BLAKELY, CFP® is a financial advisor with BLAKELY FINANCIAL, INC. located at 1022 Hutton Ln., Suite 109, High Point, NC 27262. He is the founder and president of Blakely Financial, Inc.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals.

Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser.

Diversification and asset allocation programs do not assure a profit or protect against loss in declining markets, and cannot guarantee that any objective or goal will be achieved.