By Emily Promise, CFP®, CDFA®, AIF®, APMA®, CRPC®

The COVID-19 economic crisis tested the mettle of all Americans, mainly working mothers. Research shows that the pandemic’s impacts on women have been far-reaching and potentially long-lasting. Now that the U.S. economy is picking up steam, it may be more important than ever for women to re-examine their retirement planning strategies.

Effects of the COVID-19 Economy

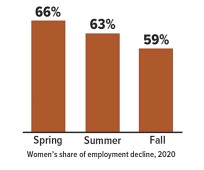

The COVID-19 recession disproportionately impacted working women because sectors that typically employ them — including retail, hospitality, and health care — were hit harder than others. As noted in a paper released by the National Bureau of Economic Research, “Employment fell more for women compared to men at every stage during the pandemic, with the biggest gender differences estimated for married women with children.” Many women were forced to cut work hours or leave jobs entirely to care for family members and supervise remote schooling activities when daycares and schools shut down.1

In a Pew Research study, 64% of women said they or someone in their household lost a job or took a pay cut during the pandemic, and nearly a quarter took unpaid time off for personal, family, or medical reasons. Half of women ranked their financial situation as “only fair” or “poor.”2

Retirement at Risk?

When it comes to retirement savings, unmarried women have the most ground to cover, according to an Employee Benefit Research Institute survey. Nearly six in 10 have less than $50,000 set aside for retirement; 31% have saved less than $1,000.3

Couple these statistics with the retirement planning challenges women faced even before the pandemic — longer life spans and lower earnings and Social Security benefits, on average — and it’s apparent that women need a carefully considered retirement strategy that will help them pursue their goals.

Making Up Lost Ground

If you or a loved one need to make up lost ground, consider the following tips.

1. Save as much as possible in tax-advantaged investment vehicles, such as employer-based retirement plans and IRAs. In 2021, you can contribute up to $19,500 to 401(k) and similar plans and $6,000 to IRAs. Those figures jump to $26,000 and $7,000, respectively, if you are 50 or older. If your employer offers a match, be sure to contribute at least enough to take full advantage of it. If you have no income but you’re married and file a joint income tax return, you can still contribute to a spousal IRA in your name, provided your spouse earns at least as much as you contribute.

2. Familiarize yourself with basic investing principles: dollar-cost averaging, diversification, and asset allocation. Dollar-cost averaging involves continuous investments in securities, regardless of fluctuating prices, and can be an effective way to accumulate shares to help meet long-term goals. However, you should consider your financial ability to continue making purchases during periods of low and high price levels. (If you contribute to an employer-based plan, you’re already using dollar-cost averaging.) Diversification and asset allocation are methods to help manage investment risk while building a portfolio appropriate for your needs. Note that all investment involves risk, and none of these strategies guarantees a profit or protects against investment loss.

3. Seek guidance from your financial professional, who can provide an objective opinion during challenging times and may be able to help you find ways to reduce costs and save more. Although there is no assurance that working with a financial professional will improve investment results, a professional can evaluate your objectives and available resources and help you consider appropriate long-term financial strategies.

This material has been provided for general informational purposes only and does not constitute either tax or legal advice. Although we go to great lengths to make sure our information is accurate and useful, we recommend you consult a tax preparer, professional tax advisor, or lawyer.

Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other specialized advice we can provide towards your financial well-being.

EMILY PROMISE is a financial advisor with BLAKELY FINANCIAL, INC. located at 1022 Hutton Ln., Suite 109, High Point, NC 27262 and can be reached at (336) 885-2530.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals.

Securities and advisory services offered through Commonwealth Financial Network, Member FINRA/SIPC, a Registered Investment Adviser.

Prepared by Commonwealth Financial Network®