Achieving financial freedom is a goal for many, but for women, it often comes with unique challenges. From wage gaps and career breaks to planning for longer life expectancies, women face distinct hurdles in their financial journeys. However, with the right knowledge, these obstacles can be overcome. In this blog, learn how to build wealth, take control of your financial future, and thrive in the financial world.

Understanding the Unique Challenges

The first step in gaining financial freedom as a woman is to understand the unique challenges you may face in the financial world. Here are a few you may come across:

Wage Gaps: Women often face wage disparities across various sectors and industries, which can significantly impact their long-term financial health.

Career Breaks Many women take career breaks for caregiving, which can impact their earning potential and career growth.

Longer Life Expectancies: Women typically live longer than men, which means it is crucial to plan for extra years of retirement.

Combating Challenges

While these challenges are very common among women, they can also be overcome. To combat wage gaps, women should be educated about industry salary standards and negotiation skills to ensure they are fairly compensated for their work. Additionally, supporting women’s access to leadership training and mentorship can help them reach higher-paying positions and close the wage gap.

Women can mitigate the financial impact of career breaks by engaging in proactive financial planning, such as saving specifically for this purpose. When speaking with your financial advisor, let them know this is part of your plan and they will help you factor it into your financial game plan.

When taking longer life expectancies into consideration, women should focus on extending their retirement planning to ensure they save enough to cover these additional years. Investing in robust healthcare plans and health savings accounts can address the rising medical costs associated with aging.

Essential Financial Strategies

When embarking on your journey toward financial independence, there are a few essential financial strategies to keep in mind:

Investing Early: Starting your investment journey early maximizes the benefit of compounding interest, which is crucial for building long-term wealth. Even small investments can accumulate significantly over time, helping women secure their financial future.

Diversified Portfolio: A mix of assets can manage risks and promote steady growth, safeguarding wealth against unpredictable market conditions. A diverse portfolio may include stocks across different industries and risk profiles, as well as other assets such as bonds and real estate.

Retirement Planning: Retirement planning is particularly important for women due to longer life expectancies and unique career trajectories. Effective strategies include maximizing 401(k) contributions and selecting suitable retirement accounts to ensure financial stability in later years. Be sure to research your employer’s retirement plan options and work with your financial advisor to select the one that best fits your unique situation and needs.

Learn and Grow

The journey to financial freedom is ongoing, requiring continuous learning, growth, and support. The following are key to a successful financial future:

Education & Awareness: Understanding the financial landscape is crucial for achieving financial independence. By educating yourself through workshops, webinars, and resources, you can become more aware and better prepared for any situation coming your way. Additionally, learning negotiation skills can help you secure better salaries and benefits, which is essential for building long-term wealth.

Strategic Planning: Strategic financial planning is essential for reaching financial independence. For example, having a plan that accounts for career interruptions by saving for sabbaticals or considering career break insurance can help create a solid path toward financial stability and independence.

Support and Community: Building a strong support system is crucial for women’s financial success. Engaging in mentorship programs for guidance and joining networks with other women facing similar financial challenges can provide valuable support.

With determination and the proper resources, women can confidently navigate their financial paths and achieve lasting financial security. If you want to learn how to gain financial independence, contact us today. We’re here to guide you every step of the way.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Retirement planning is a journey spanning the entirety of your career, evolving as you move through different phases of your life. For dads, this process holds unique significance – not only are you securing your own future, but you’re also safeguarding your family’s long-term financial well-being. From the early days of your career to the time you decide to retire, every stage of your journey offers opportunities to optimize your retirement planning strategy. As Father’s Day approaches, let’s explore retirement planning for dads and what this may look like at each career stage, ensuring a smooth transition to a financially secure retirement for you and your family.

Early Career (20s to Early 30s)

In the early stages of your career, when you are in your 20s to early 30s, time is your greatest ally. To build a strong foundation in your retirement planning, you will want to begin contributing to your retirement accounts as soon as possible. Research any retirement accounts offered by your employer and be sure to enroll in one, such as an employer’s 401(k) plan. Once enrolled, strive to contribute enough to qualify for the full employer match, if it is available, as it essentially offers free money towards your retirement savings. Simultaneously, it’s essential to establish an emergency fund, which serves as a financial buffer during unexpected situations and emergencies. Aim to have three to six months’ worth of expenses saved in this account to avoid dipping into your retirement savings and preserve future compounding gains in case of emergency.

Mid-Career (Mid-30s to 40s)

As you progress into your mid-career in your mid-30s to 40s, your earning power typically increases, making it the perfect time to ramp up your retirement contributions! Strive to max out your 401(k) contributions and consider opening an IRA for additional tax-advantaged savings. Additionally, it is critical to start diversifying your investment portfolio beyond standard retirement accounts. Other assets may include real estate, stocks, and more. Talk to your financial advisor to see which options are best for you and your risk tolerance. Moreover, while it is tempting to focus solely on saving for your children’s education during these years, it is important to maintain a balance between funding their college accounts and boosting your retirement savings.

Late Career (50s to Early 60s)

When you reach your 50s to early 60s and retirement begins to inch closer, take full advantage of catch-up contributions in your 401(k) and IRA, which allow you to contribute additional funds if you are over 50. It is also important to reevaluate your retirement goals once you reach this stage. Ask yourself, “Am I on track to live comfortably?” and adjust your savings strategies accordingly. Additionally, focus on reducing or eliminating any outstanding debt including your mortgage, credit cards, and personal loans before retirement. Entering your retirement debt-free can significantly reduce your monthly expenses as well as financial stress.

Nearing Retirement (Late 60s and beyond)

In the years closest to retirement, develop a strategic plan for withdrawing from your retirement savings accounts to maximize your gains and minimize taxes. Speak with your financial advisor to learn more about tax-saving strategies and the best approach for you and your unique situation. In addition, consider any necessary lifestyle changes such as downsizing your home for cost efficiency, and begin to plan for healthcare needs. Understand your Medicare options and assess the need for supplemental policies or long-term care insurance, ensuring you are covered for any health issues that may arise during retirement.

As you navigate the joys of fatherhood, remember it’s also crucial to plan for your future. At Blakely Financial, we’re dedicated to helping dads at every stage of fatherhood work toward a comfortable retirement. From your first Father’s Day to enjoying your golden years, let’s make sure your financial plans are as strong as the legacy you’re building. Contact us today to get started.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

529 plans are no longer solely reserved for college tuition. Today, these versatile accounts offer a broader spectrum of possibilities beyond saving for college, covering expenses like vocational schools and K-12 education. With their tax advantages and adaptability to diverse educational paths, 529 plans emerge as a strategic solution for families seeking flexibility and foresight in securing their children’s educational future. In this blog, we are rethinking the possibilities of 529 plans to explore their full potential and delving into how you can leverage these accounts to invest in your child’s future at every stage of their education journey.

529 Plans for College Tuition

Traditionally, 529 plans have been used to save for college tuition and related expenses. These accounts offer tax-deferred growth and tax-free withdrawals when funds are used for qualified higher education expenses. By contributing to a 529 plan, parents can build a dedicated fund to cover the cost of tuition, room and board, books, and other college-related expenses. Anyone can contribute to 529 plans, allowing family and friends to contribute to your child’s future education.

K-12 Tuition

In recent years, the scope of 529 plans has expanded to include K-12 education expenses. Families can now use a 529 plan to pay for up to $10,000 in tuition at elementary, middle, and high schools, including private and religious institutions. This flexibility allows parents to start saving for their child’s education from an early age and provides additional options for educational choices beyond the traditional public school system.

Vocational Schools

Another exciting development in the possibilities of 529 plans is the ability to use funds for vocational schools and career training programs. If your child is interested in pursuing a trade or obtaining specialized certifications, a 529 plan can help cover the cost of tuition, fees, and supplies. This opens up new opportunities for students who may not have considered traditional four-year college programs, allowing them to pursue career paths aligned with their interests and goals. Eligible vocational schools, including many technical colleges, cosmetology schools, culinary schools, and more can be found using the Federal School Code Lookup Tool.

Apprenticeship Programs

529 plans can also be used to support apprenticeship programs that are certified and registered with the U.S. Department of Labor’s National Apprenticeships Act, providing financial assistance for on-the-job training and educational coursework. Apprenticeships offer a valuable alternative to traditional education pathways, allowing individuals to earn, while they learn and gain practical skills in a specific trade or industry. By using funds from a 529 plan, apprentices can offset the cost of program fees, books, supplies, equipment, and other related expenses, making these opportunities more accessible to aspiring professionals. The Department of Labor provides a search tool to determine whether your apprenticeship is eligible for 529 plan funds.

As 529 Day approaches, it’s time to rethink the possibilities of 529 plans and explore the various ways you can use them to invest in your child’s education journey. Contact the Blakely Financial office today to learn how we can help you maximize the benefits of 529 plans and support your child’s goals every step of the way.

The fees, expenses, and features of 529 plans can vary from state to state. 529 plans involve investment risk, including the possible loss of funds. There is no guarantee that an education-funding goal will be met. In order to be federally tax free, earnings must be used to pay for qualified education expenses. The earnings portion of a nonqualified withdrawal will be subject to ordinary income tax at the recipient’s marginal rate and subject to a 10 percent penalty. By investing in a plan outside your state of residence, you may lose any state tax benefits. 529 plans are subject to enrollment, maintenance, and administration/management fees and expenses.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Graduation is right around the corner! It’s an exciting time to celebrate your child’s accomplishments and look ahead to their future. As a parent, you play a crucial role in setting them up for success, and one of the best ways to do so is by investing in their future. There are countless ways to sow the seeds for long-term financial security and prosperity. In this blog, we are delving into ways you can invest in your graduate’s future journey today, so they can watch the returns flourish in years to come.

Roth IRA Contributions

Consider starting a Roth IRA for your child if they’ve earned income. A Roth IRA offers tax-free growth and withdrawals in retirement, providing a valuable tool for building financial security over the long term. By making contributions to a Roth IRA early on in your child’s life, you can leverage the power of compounding growth and set them on the path to a comfortable retirement. While Roth IRAs can also be used for educational expenses, in order to withdraw money without being charged taxes or penalties, you must be over 59 ½ years old and the account must be at least five years old.

529 College Savings Plan

Investing in a 529 college savings plan is an excellent option to support your child’s educational goals. These plans offer tax-free growth and withdrawals for qualified education expenses, making them a tax-efficient way to save for college. Parents are not the only people eligible to contribute, allowing family and friends to give a lasting gift to the beneficiary’s future.

Whether your child plans to attend a traditional four-year college or university or pursue vocational training, a 529 plan can help ease the financial burden of higher education and provide valuable opportunities for their future. If your child receives a scholarship or decides against further eligible education, 529 savings plans offer the flexibility to change the beneficiary to avoid paying taxes and fees on unused savings.

Custodial Accounts (UTMA/UGMA)

Opening a custodial account, such as a Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA), allows you to invest in stocks, bonds, or mutual funds on behalf of your child. These accounts are a great investment option because they offer flexibility and control, allowing you to manage the assets until your child reaches adulthood (at 18 or 21, depending on the state). Introducing your child to the world of investing early on can help them develop valuable financial literacy skills and set them up for financial success in the years to come.

Additionally, the funds can be used for the minor’s benefit before they take control of the account, including to help pay for college! Earnings are taxed at the minor’s tax rate, subject to kiddie tax rules. Before pursuing custodial accounts, talk to a financial professional to confirm which tax rules apply and how to best manage the funds.

Financial Literacy Education

Investing in your child’s financial education is perhaps one of the most valuable investments you can make. Providing access to resources and courses on financial literacy from a young age can equip your child with the knowledge and skills necessary to manage and grow their finances effectively. From budgeting and saving to investing and retirement planning, a strong foundation in financial literacy sets the stage for a lifetime of financial success.

As graduation season approaches, now is the perfect time to start investing in your graduate’s future. Regardless of the investment options you choose, every investment you make lays the groundwork for their long-term success. By contributing to your child’s journey to financial literacy and prosperity today, you can help create a bright and prosperous future for your graduate tomorrow. If you need assistance getting started, contact Blakely Financial today. Our team is here to help you discover the best investment options and work towards a secure financial future for you and your family.

The fees, expenses, and features of 529 plans can vary from state to state. 529 plans involve investment risk, including the possible loss of funds. There is no guarantee that an education-funding goal will be met. In order to be federally tax free, earnings must be used to pay for qualified education expenses. The earnings portion of a nonqualified withdrawal will be subject to ordinary income tax at the recipient’s marginal rate and subject to a 10 percent penalty. By investing in a plan outside your state of residence, you may lose any state tax benefits. 529 plans are subject to enrollment, maintenance, and administration/management fees and expenses.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

As we recognize Financial Literacy Month, we must assess our knowledge and understanding of key financial concepts that impact our daily lives such as budgeting, investing, borrowing, and more. Whether you’re a seasoned investor or just beginning your financial journey, this quiz offers an opportunity to reflect on your financial knowledge and take steps toward improving your financial literacy. Are you ready to see where you stand? Dive into our Financial Literacy Month quiz and put your knowledge to the test!

What is the effect of compound interest on an investment over time?

Decreases the total amount of interest earned

Increases the total amount of interest earned by adding interest to the principal and accumulated interest

Has no effect on the total amount of interest earned

Only applies to savings accounts

Correct Answer: 2

Compound interest allows you to earn interest not only on the initial principal amount invested but also on the accumulated interest from previous periods. Over time, this compounding effect results in the exponential growth of your investment, significantly increasing the total amount of interest earned.

Why is diversification important in an investment portfolio?

It guarantees a fixed return on investment

It reduces risk by spreading investments across various asset classes

It focuses investment in one sector to maximize returns

It ensures all investments will profit

Correct Answer: 2

The process of diversification involves spreading your investments across different asset classes to minimize risk. These may include stocks, bonds, and real estate. By diversifying your investment portfolio, you can mitigate the impact of adverse events affecting any single asset or sector. This will help stabilize returns and potentially improve long-term performance. If you’re struggling to diversify your investments, meet with your financial advisor to discuss your options.

Which of the following accounts offers tax-deferred growth?

Checking account

Certificate of Deposit (CD)

401(k) or Traditional IRA

Brokerage Account

Correct Answer: 3

Tax-deferred growth refers to the ability of investments to grow without being taxed until withdrawal. Both 401(k) plans and Traditional IRAs offer tax-deferred growth, allowing your investments to compound over time without being subject to immediate taxation on earnings. Everyone’s financial situation is unique, so be sure to talk to your financial advisor to be sure you are taking advantage of the best plans and accounts for you.

What is a “bull market”?

A market characterized by declining stock prices

A market in which stock prices are remaining stable

A market characterized by rising stock prices

A market that exclusively trades in agricultural stocks

Correct Answer: 3

A bull market is a period characterized by rising stock prices and investor optimism. During a bull market, investor confidence is high, leading to increased buying activity and upward momentum in stock prices across the market.

What does a fixed-rate mortgage offer that a variable-rate mortgage does not?

A mortgage rate that changes with the market

Lower interest rates over the life of the loan

The same interest rate and monthly payment throughout the life of the loan

Higher borrowing limits

Correct Answer: 3

A fixed-rate mortgage offers borrowers the security of a consistent, or fixed, interest rate and monthly payment throughout the life of the loan. In contrast, a variable-rate mortgage will have interest rates that fluctuate with market conditions, resulting in varying monthly payments and potentially higher levels of financial uncertainty for borrowers. Talk to your financial advisor to sort out which option is best for you and your financial health.

Whether you aced every question and passed with flying colors or found new areas to explore, taking the time to assess your financial literacy is a valuable step toward financial empowerment. Remember, financial literacy is an ongoing journey, and there’s always room to learn and grow.

If you found any questions throughout the quiz challenging or would like to delve deeper into any topics, contact the Blakely Financial team today. We are ready to help you navigate your financial journey with confidence! For additional resources and insights designed to boost your financial understanding, check out the Blakely Financial website.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Stocks continued their upward trajectory in early 2024. The S&P 500 returned more than 10% for a second consecutive quarter, setting multiple new all-time highs along the way. Notably, this quarter saw a significant shift in sentiment, as investors now only expect three interest rate cuts this year as compared to six at the start of the year. This change in expectations came as inflation progress slowed and the U.S. economy continued to expand despite higher interest rates, both of which signal a need for fewer rate cuts. This letter recaps the first quarter, discusses the stock market’s strong start to 2024, and looks ahead to the second quarter.

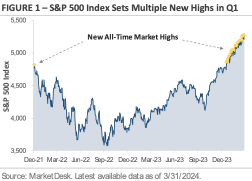

S&P 500 Sets 22 New All-Time Highs in Q1

The stock market is off to a strong start this year, with the S&P 500 Index gaining +10.4% in the first quarter. Figure 1 graphs the price of the S&P 500 Index since the end of 2021. The yellow dots mark new all-time closing highs. On the far-left side of the chart, the single yellow dot marks the previous all-time closing high set on January 3rd, 2022. Shortly after the January 2022 all-time high, the Federal Reserve started its campaign of aggressive interest rate hikes as inflation spiked to a 40-year high. The chart shows the 2022 stock market selloff as investors feared that higher interest rates would slow the economy.

The January 2022 all-time closing high held throughout all of 2022 and 2023, but it’s already been eclipsed multiple times in 2024. After trading below its prior all-time high for over two years, the S&P 500 Index has set 22 new all-time closing highs this year. The yellow dots on the far-right side of the chart mark these new highs and show the S&P 500’s steady climb higher in early 2024.

Inflation Progress Slowed in Q1

Inflation was on a steady downward trend heading into this year, and the market expected it to continue moving lower. However, recent data is causing investors to rethink that assumption. Figure 2 graphs the year-over-year change in the Consumer Price Index, which measures the change in price for a basket of consumer goods. The chart shows the inflation spike in 2021 and early 2022, followed by a period of easing inflation during the past two years. However, the yellow box shows that the pace of inflation progress has slowed recently. While inflation is still drifting lower, it’s not falling as quickly as investors or the Federal Reserve want.

The question is whether the slowing progress is the start of a new trend or a temporary break in the current trend. Seasonality may be contributing to the slowdown, as inflation tends to be higher earlier in the year and then lower later in the year. Is the early 2024 rise the result of previously agreed upon contractual price increases, or does it hint at something more under the surface? Federal Reserve Chair Jerome Powell believes the early 2024 inflation bump is seasonal and short-term in nature. The market is less certain and more divided.

The chart also demonstrates that getting back to the Fed’s 2% inflation target will be bumpy and uneven. The disinflation process won’t be a straight line. The latest risk is rising oil prices, with the price of a regular gallon of gasoline jumping by over +20% during Q1. Falling energy prices helped to ease inflation pressures during the past two years, but there is now a question about whether that trend can continue with gas prices rising.

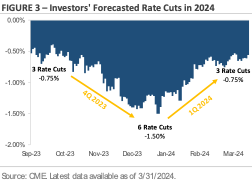

Investors Expect Fewer Interest Rate Cuts This Year

One of the big debates heading into 2024 was how many times the Federal Reserve would cut interest rates. Figure 3 tracks the market’s rate cut forecast. Looking back to the start of Q4 2023, the market expected the Federal Reserve to cut interest rates by -0.75% this year. By the end of December, the market’s rate cut forecast for the entirety of 2024 had risen to -1.50%. Based on a typical rate cut increment of -0.25%, investors came into this year expecting six interest rate cuts (i.e., -1.50% in total cuts). In contrast, the Federal Reserve only expected three interest rate cuts at the start of this year, or half the market’s estimate. There was a debate over whose interest rate cut forecast was more accurate. As of the end of Q1, the central bank’s forecast appears more accurate. Investors now only expect three interest rate cuts this year, which is in line with the Fed’s initial forecast.

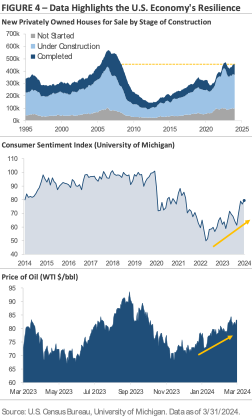

Why do investors expect fewer interest rate cuts this year? One reason is that inflation progress is slowing. Another reason is that the U.S. economy remains resilient despite higher rates. Figure 4 graphs three data points that underscore this resilience. The top chart graphs the number of new homes for sale by stage of construction: not started; under construction; and completed. The chart shows home construction activity is at levels not seen since before the 2008 financial crisis, despite the average 30-year fixed-rate mortgage sitting near a 15-year high of 7%. The middle section shows consumer sentiment rose to a 2.5-year high in March after setting a record low in June 2022. Multiple factors are contributing to the improved sentiment, including a tight labor market, rising stock prices and home values, expectations for a continued decline in inflation, and a solid economic backdrop. The bottom chart tracks the price of a barrel of West Text Intermediate crude. Crude oil prices have risen from approximately $70 per barrel at the start of the year to $83 per barrel at the end of Q1, an increase of roughly +18.5%. Oil is a cyclical commodity, so rising oil prices suggest demand is strong and may hint at underlying strength in the U.S. economy.

Equity Market Recap – Stocks Post a Second Consecutive Quarter of Strong Gains

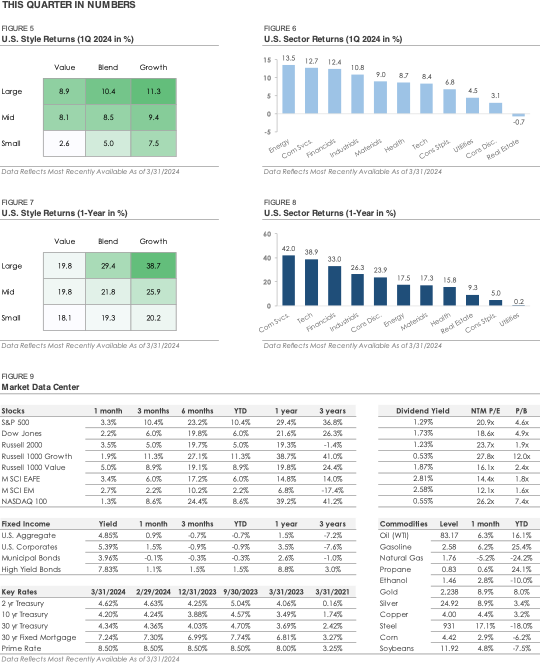

The opening section discussed the stock market’s strong start to the year. Following an impressive +11.6% gain in Q4, the S&P 500 returned +10.4% in Q1. Small cap stocks underperformed during the quarter, as the Russell 2000 Index returned +5.0%. Ten of the eleven S&P 500 sectors posted gains, with cyclical sectors outperforming their defensive counterparts. The energy, financial, and industrial sectors each outperformed the broader S&P 500 Index, while the real estate, utility, and consumer staple sectors underperformed as the stock market rallied.

International stocks underperformed U.S. stocks for a fourth consecutive quarter during Q1. Over the past twelve months, the MSCI EAFE Index of developed market stocks has returned +14.8%, or roughly half of the S&P 500’s +29.4% return. The MSCI Emerging Market Index has returned only +6.8%, or approximately one-fourth of the S&P 500. A few themes may explain why international stocks continue to underperform. First, international stock market indices lack exposure to leading artificial intelligence companies like Microsoft, Nvidia, and Super Micro Computer. Second, as discussed above, the U.S. economy continues to expand despite higher rates. In contrast, some countries and regions outside the U.S. are already feeling the impact of higher interest rates. Investors have been attracted to the U.S. for both its AI exposure and relative economic strength.

Credit Market Recap – Bonds Trade Lower After a Strong Fourth Quarter

While stocks started the year off with strong gains, bonds traded lower during Q1. The losses came as investors realized that the continued resilience of the U.S. economy meant the Federal Reserve may not need to cut interest rates as much, which caused Treasury yields to rise. The Bloomberg U.S. Bond Aggregate Index, which tracks a broad index of investment-grade rated bonds, posted a total return of -0.7%. It was a sharp reversal from Q4, when the index posted its first quarterly gain since Q1 2023 and its biggest quarterly gain since 1989.

In the corporate bond category, investment-grade bonds underperformed high-yield bonds during Q1. Over the past twelve months, high-yield corporate bonds have generated a total return of +8.8%, which factors in the interest payments received. Investment-grade corporate bonds generated a +3.5% total return over the same period. The high-yield bond universe continues to benefit from multiple themes. First, the group yields 7.83% at the end of Q1, which is 2.45% higher than investment-grade bonds. This extra yield helps boost high-yield’s total return. Second, as Figure 4 highlights, the U.S. economy has remained resilient despite higher interest rates. With the U.S. economy expanding at a solid pace, high-yield bonds’ credit risk has remained stable, limiting the number of defaults.

Second Quarter Outlook – Themes to Watch

The big investment themes were mostly unchanged during the first quarter. Stocks continued to trade higher, and the U.S. economy remained in expansion mode. While the market now expects fewer interest rate cuts this year, the primary reason is that investors and the Fed believe the U.S. economy can handle higher interest rates. Economic theory suggests that higher interest rates should slow economic activity as the cost of capital increases, but the data tells a different story this cycle. Home construction activity is the strongest since before 2008, consumer sentiment recently hit a 2.5-year high, and unemployment remains below 4%.

It’s difficult to overstate the uniqueness of this economic cycle. There was unprecedented monetary and fiscal stimulus in 2020 and 2021, followed by a rapid rise in interest rates in 2022 and 2023 as inflation reached levels not seen since the 1970s. In the housing market, many homeowners locked in low mortgage rates during the past few years, which has effectively limited the impact of rising interest rates. The labor market remains relatively tight after five million workers left the labor force during the pandemic and didn’t return, which has not been seen before. These themes won’t reverse quickly and will have long-lasting impacts, which both the Federal Reserve and markets must navigate. We will continue to monitor financial markets and the economy, provide timely updates to you, and adjust portfolios as needed.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation

All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.

April is Financial Literacy Month, a time dedicated to empowering everyone with the knowledge necessary to make informed and effective financial decisions. There are many ways to improve your financial literacy, and we are thrilled to share some of our favorite resources to boost your financial wisdom. As a listener of the following podcasts, you’ll gain valuable insights from experts, hear real-life stories, and listen in on thought-provoking discussions on a wide range of financial topics.

Planet Money

Our first highlight is Planet Money, a podcast by NPR that makes economics fun, understandable, and relevant. The podcast can take any topic and relate it back to the economy, helping you understand both the economy and the world as a whole.

Episodes are typically around 30 minutes or less. Here are some recent examples of episodes we’ve enjoyed:

Planet Money can be found anywhere you listen to your podcasts!

BiggerPockets

Dive into the world of finance, entrepreneurship, and real estate with our next podcast pick: BiggerPockets. Whether you’re a seasoned investor or just getting started, BiggerPockets offers invaluable insights to help you build your wealth and navigate the complexities of real estate investment.

Most episodes are less than 1 hour long. Here are some recent episodes we enjoyed:

BiggerPockets is available anywhere you listen to your podcasts!

Bloomberg’s Masters in Business

Our next feature is Bloomberg’s Masters in Business. This podcast brings the insights of the world’s leading business minds right to your ears. Delve into deep conversations with industry pioneers in finance, economics, and beyond. Discover the strategies and stories behind successful business ventures, elevating your understanding and inspiring you with every episode.

Episodes vary in length, ranging from just 5 minutes to over an hour long. Here are some episodes we’ve enjoyed recently:

Masters in Business is available wherever you listen to podcasts!

Exploring podcasts during Financial Literacy Month offers an engaging and accessible way to expand your financial knowledge and empower yourself to make informed decisions about your finances. Whether you’re looking to improve your budgeting skills, learn about investing, or gain a deeper understanding of economic concepts, these podcasts provide valuable resources to help you navigate your financial journey with confidence. Grab your headphones and start listening – your healthy financial future awaits!

For more personalized advice and insights, contact the Blakley Financial team today. Our advisors are available and ready to assist you in your journey toward strong financial literacy and well-being.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Embarking on the journey of blended families brings both joy and unique challenges. Navigating the intricacies of a blended family requires careful consideration and planning, especially when it comes to managing finances. No matter your age or stage in life, open communication, and proactive financial strategies are essential for building a strong foundation for your new family’s future finances. In this blog, we’ll explore key considerations for managing finances in a blended family to set the stage for a prosperous and harmonious financial future.

Blended Family Basics

When entering into a blended family, there are some key items to consider to help navigate potential challenges. Above all, clear communication is paramount.

Clear communication is not only about how you’ll blend your children if you have kids in your marriage but also about how you will manage your finances in this new blended situation. It is important to ensure your wishes are clear to both families within a blended family so they are played out properly in the long run. Having clear communication across a variety of different areas within your life will make the financial planning process as seamless as possible.

Blended Family Estate Planning

Managing estate planning in blended families can present unique challenges. When entering into a blended family, it is critical to sit down with your new spouse to discuss several important topics, including estate planning. Estate planning is important and can be challenging for everyone, but there can be some additional difficulties and hurdles when it comes to entering a blended family.

You need to have an honest conversation regarding what would happen if something were to happen to you. This does not only include death. If one of you were to get sick, who is going to make medical decisions for you? Who is going to be able to cash your checks, manage your investment accounts with your advisor, and have that financial power of attorney? In the instance that you were to pass away, it is important to consider where you want your assets divided. Will they go to your new spouse, prior children, or somewhere else?

While these conversations may be difficult, they are necessary to have with your new spouse when entering a blended family. If you need help getting started with these, reach out to your financial advisor. They will have resources available to help guide you through the estate planning process.

Merge or Keep Separate?

Again, upfront conversations with your new spouse may be uncomfortable but are necessary so you are on the same page heading for a successful future. Your finances should be part of these conversations, particularly whether you will keep your finances separate or merge them. We’ve seen success both ways, the decision really depends on how you both want to work.

If you do opt for separate accounts, you will want to be sure to have beneficiary designations on those accounts, have payable on death on your bank accounts, and any other necessary precautions in place so that if something were to happen to one of you, the other would still have access to important accounts. One common approach is to have one house account where you both contribute money to cover joint bills, but then keep your separate accounts for your own mad money. Regardless of what this decision will look like for you, clear communication is key to finding a balance that works for both partners.

Finding Your Unique Advisor

When entering into a blended family situation, no matter what your age is, you must find a financial advisor who caters to your unique needs. If you’re further along in your career, you may already have established financial habits long before you entered into this new marriage, making it even more important to find an advisor who can work with you to help you reach your unique goals in the long term.

Blakely Financial’s own Emily Promise is a Certified Divorce Financial Analyst, CDFA®, Institute for Divorce Financial Analysts. With her experience, she can help guide you and your blended family toward a bright financial future together. Contact us today to get started.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.