As we recognize Financial Literacy Month, we must assess our knowledge and understanding of key financial concepts that impact our daily lives such as budgeting, investing, borrowing, and more. Whether you’re a seasoned investor or just beginning your financial journey, this quiz offers an opportunity to reflect on your financial knowledge and take steps toward improving your financial literacy. Are you ready to see where you stand? Dive into our Financial Literacy Month quiz and put your knowledge to the test!

What is the effect of compound interest on an investment over time?

Decreases the total amount of interest earned

Increases the total amount of interest earned by adding interest to the principal and accumulated interest

Has no effect on the total amount of interest earned

Only applies to savings accounts

Correct Answer: 2

Compound interest allows you to earn interest not only on the initial principal amount invested but also on the accumulated interest from previous periods. Over time, this compounding effect results in the exponential growth of your investment, significantly increasing the total amount of interest earned.

Why is diversification important in an investment portfolio?

It guarantees a fixed return on investment

It reduces risk by spreading investments across various asset classes

It focuses investment in one sector to maximize returns

It ensures all investments will profit

Correct Answer: 2

The process of diversification involves spreading your investments across different asset classes to minimize risk. These may include stocks, bonds, and real estate. By diversifying your investment portfolio, you can mitigate the impact of adverse events affecting any single asset or sector. This will help stabilize returns and potentially improve long-term performance. If you’re struggling to diversify your investments, meet with your financial advisor to discuss your options.

Which of the following accounts offers tax-deferred growth?

Checking account

Certificate of Deposit (CD)

401(k) or Traditional IRA

Brokerage Account

Correct Answer: 3

Tax-deferred growth refers to the ability of investments to grow without being taxed until withdrawal. Both 401(k) plans and Traditional IRAs offer tax-deferred growth, allowing your investments to compound over time without being subject to immediate taxation on earnings. Everyone’s financial situation is unique, so be sure to talk to your financial advisor to be sure you are taking advantage of the best plans and accounts for you.

What is a “bull market”?

A market characterized by declining stock prices

A market in which stock prices are remaining stable

A market characterized by rising stock prices

A market that exclusively trades in agricultural stocks

Correct Answer: 3

A bull market is a period characterized by rising stock prices and investor optimism. During a bull market, investor confidence is high, leading to increased buying activity and upward momentum in stock prices across the market.

What does a fixed-rate mortgage offer that a variable-rate mortgage does not?

A mortgage rate that changes with the market

Lower interest rates over the life of the loan

The same interest rate and monthly payment throughout the life of the loan

Higher borrowing limits

Correct Answer: 3

A fixed-rate mortgage offers borrowers the security of a consistent, or fixed, interest rate and monthly payment throughout the life of the loan. In contrast, a variable-rate mortgage will have interest rates that fluctuate with market conditions, resulting in varying monthly payments and potentially higher levels of financial uncertainty for borrowers. Talk to your financial advisor to sort out which option is best for you and your financial health.

Whether you aced every question and passed with flying colors or found new areas to explore, taking the time to assess your financial literacy is a valuable step toward financial empowerment. Remember, financial literacy is an ongoing journey, and there’s always room to learn and grow.

If you found any questions throughout the quiz challenging or would like to delve deeper into any topics, contact the Blakely Financial team today. We are ready to help you navigate your financial journey with confidence! For additional resources and insights designed to boost your financial understanding, check out the Blakely Financial website.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Stocks continued their upward trajectory in early 2024. The S&P 500 returned more than 10% for a second consecutive quarter, setting multiple new all-time highs along the way. Notably, this quarter saw a significant shift in sentiment, as investors now only expect three interest rate cuts this year as compared to six at the start of the year. This change in expectations came as inflation progress slowed and the U.S. economy continued to expand despite higher interest rates, both of which signal a need for fewer rate cuts. This letter recaps the first quarter, discusses the stock market’s strong start to 2024, and looks ahead to the second quarter.

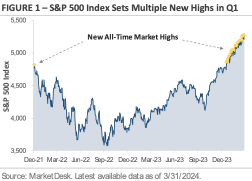

S&P 500 Sets 22 New All-Time Highs in Q1

The stock market is off to a strong start this year, with the S&P 500 Index gaining +10.4% in the first quarter. Figure 1 graphs the price of the S&P 500 Index since the end of 2021. The yellow dots mark new all-time closing highs. On the far-left side of the chart, the single yellow dot marks the previous all-time closing high set on January 3rd, 2022. Shortly after the January 2022 all-time high, the Federal Reserve started its campaign of aggressive interest rate hikes as inflation spiked to a 40-year high. The chart shows the 2022 stock market selloff as investors feared that higher interest rates would slow the economy.

The January 2022 all-time closing high held throughout all of 2022 and 2023, but it’s already been eclipsed multiple times in 2024. After trading below its prior all-time high for over two years, the S&P 500 Index has set 22 new all-time closing highs this year. The yellow dots on the far-right side of the chart mark these new highs and show the S&P 500’s steady climb higher in early 2024.

Inflation Progress Slowed in Q1

Inflation was on a steady downward trend heading into this year, and the market expected it to continue moving lower. However, recent data is causing investors to rethink that assumption. Figure 2 graphs the year-over-year change in the Consumer Price Index, which measures the change in price for a basket of consumer goods. The chart shows the inflation spike in 2021 and early 2022, followed by a period of easing inflation during the past two years. However, the yellow box shows that the pace of inflation progress has slowed recently. While inflation is still drifting lower, it’s not falling as quickly as investors or the Federal Reserve want.

The question is whether the slowing progress is the start of a new trend or a temporary break in the current trend. Seasonality may be contributing to the slowdown, as inflation tends to be higher earlier in the year and then lower later in the year. Is the early 2024 rise the result of previously agreed upon contractual price increases, or does it hint at something more under the surface? Federal Reserve Chair Jerome Powell believes the early 2024 inflation bump is seasonal and short-term in nature. The market is less certain and more divided.

The chart also demonstrates that getting back to the Fed’s 2% inflation target will be bumpy and uneven. The disinflation process won’t be a straight line. The latest risk is rising oil prices, with the price of a regular gallon of gasoline jumping by over +20% during Q1. Falling energy prices helped to ease inflation pressures during the past two years, but there is now a question about whether that trend can continue with gas prices rising.

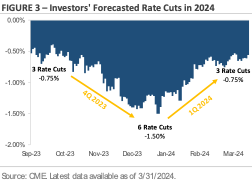

Investors Expect Fewer Interest Rate Cuts This Year

One of the big debates heading into 2024 was how many times the Federal Reserve would cut interest rates. Figure 3 tracks the market’s rate cut forecast. Looking back to the start of Q4 2023, the market expected the Federal Reserve to cut interest rates by -0.75% this year. By the end of December, the market’s rate cut forecast for the entirety of 2024 had risen to -1.50%. Based on a typical rate cut increment of -0.25%, investors came into this year expecting six interest rate cuts (i.e., -1.50% in total cuts). In contrast, the Federal Reserve only expected three interest rate cuts at the start of this year, or half the market’s estimate. There was a debate over whose interest rate cut forecast was more accurate. As of the end of Q1, the central bank’s forecast appears more accurate. Investors now only expect three interest rate cuts this year, which is in line with the Fed’s initial forecast.

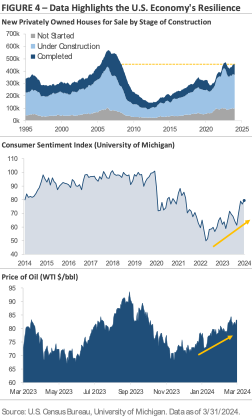

Why do investors expect fewer interest rate cuts this year? One reason is that inflation progress is slowing. Another reason is that the U.S. economy remains resilient despite higher rates. Figure 4 graphs three data points that underscore this resilience. The top chart graphs the number of new homes for sale by stage of construction: not started; under construction; and completed. The chart shows home construction activity is at levels not seen since before the 2008 financial crisis, despite the average 30-year fixed-rate mortgage sitting near a 15-year high of 7%. The middle section shows consumer sentiment rose to a 2.5-year high in March after setting a record low in June 2022. Multiple factors are contributing to the improved sentiment, including a tight labor market, rising stock prices and home values, expectations for a continued decline in inflation, and a solid economic backdrop. The bottom chart tracks the price of a barrel of West Text Intermediate crude. Crude oil prices have risen from approximately $70 per barrel at the start of the year to $83 per barrel at the end of Q1, an increase of roughly +18.5%. Oil is a cyclical commodity, so rising oil prices suggest demand is strong and may hint at underlying strength in the U.S. economy.

Equity Market Recap – Stocks Post a Second Consecutive Quarter of Strong Gains

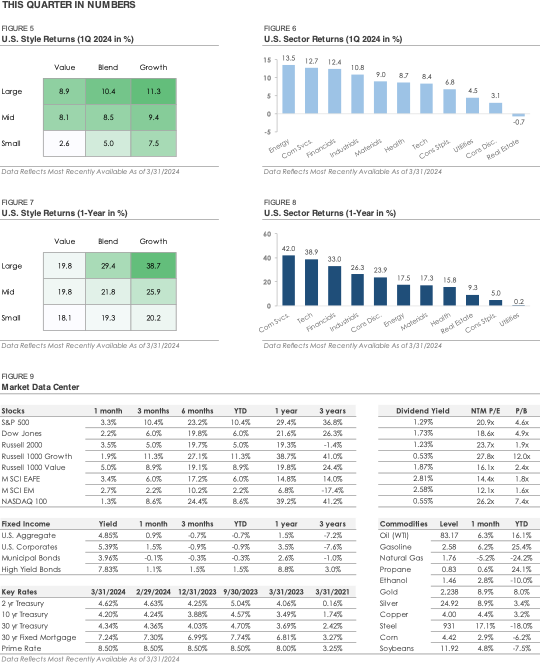

The opening section discussed the stock market’s strong start to the year. Following an impressive +11.6% gain in Q4, the S&P 500 returned +10.4% in Q1. Small cap stocks underperformed during the quarter, as the Russell 2000 Index returned +5.0%. Ten of the eleven S&P 500 sectors posted gains, with cyclical sectors outperforming their defensive counterparts. The energy, financial, and industrial sectors each outperformed the broader S&P 500 Index, while the real estate, utility, and consumer staple sectors underperformed as the stock market rallied.

International stocks underperformed U.S. stocks for a fourth consecutive quarter during Q1. Over the past twelve months, the MSCI EAFE Index of developed market stocks has returned +14.8%, or roughly half of the S&P 500’s +29.4% return. The MSCI Emerging Market Index has returned only +6.8%, or approximately one-fourth of the S&P 500. A few themes may explain why international stocks continue to underperform. First, international stock market indices lack exposure to leading artificial intelligence companies like Microsoft, Nvidia, and Super Micro Computer. Second, as discussed above, the U.S. economy continues to expand despite higher rates. In contrast, some countries and regions outside the U.S. are already feeling the impact of higher interest rates. Investors have been attracted to the U.S. for both its AI exposure and relative economic strength.

Credit Market Recap – Bonds Trade Lower After a Strong Fourth Quarter

While stocks started the year off with strong gains, bonds traded lower during Q1. The losses came as investors realized that the continued resilience of the U.S. economy meant the Federal Reserve may not need to cut interest rates as much, which caused Treasury yields to rise. The Bloomberg U.S. Bond Aggregate Index, which tracks a broad index of investment-grade rated bonds, posted a total return of -0.7%. It was a sharp reversal from Q4, when the index posted its first quarterly gain since Q1 2023 and its biggest quarterly gain since 1989.

In the corporate bond category, investment-grade bonds underperformed high-yield bonds during Q1. Over the past twelve months, high-yield corporate bonds have generated a total return of +8.8%, which factors in the interest payments received. Investment-grade corporate bonds generated a +3.5% total return over the same period. The high-yield bond universe continues to benefit from multiple themes. First, the group yields 7.83% at the end of Q1, which is 2.45% higher than investment-grade bonds. This extra yield helps boost high-yield’s total return. Second, as Figure 4 highlights, the U.S. economy has remained resilient despite higher interest rates. With the U.S. economy expanding at a solid pace, high-yield bonds’ credit risk has remained stable, limiting the number of defaults.

Second Quarter Outlook – Themes to Watch

The big investment themes were mostly unchanged during the first quarter. Stocks continued to trade higher, and the U.S. economy remained in expansion mode. While the market now expects fewer interest rate cuts this year, the primary reason is that investors and the Fed believe the U.S. economy can handle higher interest rates. Economic theory suggests that higher interest rates should slow economic activity as the cost of capital increases, but the data tells a different story this cycle. Home construction activity is the strongest since before 2008, consumer sentiment recently hit a 2.5-year high, and unemployment remains below 4%.

It’s difficult to overstate the uniqueness of this economic cycle. There was unprecedented monetary and fiscal stimulus in 2020 and 2021, followed by a rapid rise in interest rates in 2022 and 2023 as inflation reached levels not seen since the 1970s. In the housing market, many homeowners locked in low mortgage rates during the past few years, which has effectively limited the impact of rising interest rates. The labor market remains relatively tight after five million workers left the labor force during the pandemic and didn’t return, which has not been seen before. These themes won’t reverse quickly and will have long-lasting impacts, which both the Federal Reserve and markets must navigate. We will continue to monitor financial markets and the economy, provide timely updates to you, and adjust portfolios as needed.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation

All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.

April is Financial Literacy Month, a time dedicated to empowering everyone with the knowledge necessary to make informed and effective financial decisions. There are many ways to improve your financial literacy, and we are thrilled to share some of our favorite resources to boost your financial wisdom. As a listener of the following podcasts, you’ll gain valuable insights from experts, hear real-life stories, and listen in on thought-provoking discussions on a wide range of financial topics.

Planet Money

Our first highlight is Planet Money, a podcast by NPR that makes economics fun, understandable, and relevant. The podcast can take any topic and relate it back to the economy, helping you understand both the economy and the world as a whole.

Episodes are typically around 30 minutes or less. Here are some recent examples of episodes we’ve enjoyed:

Planet Money can be found anywhere you listen to your podcasts!

BiggerPockets

Dive into the world of finance, entrepreneurship, and real estate with our next podcast pick: BiggerPockets. Whether you’re a seasoned investor or just getting started, BiggerPockets offers invaluable insights to help you build your wealth and navigate the complexities of real estate investment.

Most episodes are less than 1 hour long. Here are some recent episodes we enjoyed:

BiggerPockets is available anywhere you listen to your podcasts!

Bloomberg’s Masters in Business

Our next feature is Bloomberg’s Masters in Business. This podcast brings the insights of the world’s leading business minds right to your ears. Delve into deep conversations with industry pioneers in finance, economics, and beyond. Discover the strategies and stories behind successful business ventures, elevating your understanding and inspiring you with every episode.

Episodes vary in length, ranging from just 5 minutes to over an hour long. Here are some episodes we’ve enjoyed recently:

Masters in Business is available wherever you listen to podcasts!

Exploring podcasts during Financial Literacy Month offers an engaging and accessible way to expand your financial knowledge and empower yourself to make informed decisions about your finances. Whether you’re looking to improve your budgeting skills, learn about investing, or gain a deeper understanding of economic concepts, these podcasts provide valuable resources to help you navigate your financial journey with confidence. Grab your headphones and start listening – your healthy financial future awaits!

For more personalized advice and insights, contact the Blakley Financial team today. Our advisors are available and ready to assist you in your journey toward strong financial literacy and well-being.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Embarking on the journey of blended families brings both joy and unique challenges. Navigating the intricacies of a blended family requires careful consideration and planning, especially when it comes to managing finances. No matter your age or stage in life, open communication, and proactive financial strategies are essential for building a strong foundation for your new family’s future finances. In this blog, we’ll explore key considerations for managing finances in a blended family to set the stage for a prosperous and harmonious financial future.

Blended Family Basics

When entering into a blended family, there are some key items to consider to help navigate potential challenges. Above all, clear communication is paramount.

Clear communication is not only about how you’ll blend your children if you have kids in your marriage but also about how you will manage your finances in this new blended situation. It is important to ensure your wishes are clear to both families within a blended family so they are played out properly in the long run. Having clear communication across a variety of different areas within your life will make the financial planning process as seamless as possible.

Blended Family Estate Planning

Managing estate planning in blended families can present unique challenges. When entering into a blended family, it is critical to sit down with your new spouse to discuss several important topics, including estate planning. Estate planning is important and can be challenging for everyone, but there can be some additional difficulties and hurdles when it comes to entering a blended family.

You need to have an honest conversation regarding what would happen if something were to happen to you. This does not only include death. If one of you were to get sick, who is going to make medical decisions for you? Who is going to be able to cash your checks, manage your investment accounts with your advisor, and have that financial power of attorney? In the instance that you were to pass away, it is important to consider where you want your assets divided. Will they go to your new spouse, prior children, or somewhere else?

While these conversations may be difficult, they are necessary to have with your new spouse when entering a blended family. If you need help getting started with these, reach out to your financial advisor. They will have resources available to help guide you through the estate planning process.

Merge or Keep Separate?

Again, upfront conversations with your new spouse may be uncomfortable but are necessary so you are on the same page heading for a successful future. Your finances should be part of these conversations, particularly whether you will keep your finances separate or merge them. We’ve seen success both ways, the decision really depends on how you both want to work.

If you do opt for separate accounts, you will want to be sure to have beneficiary designations on those accounts, have payable on death on your bank accounts, and any other necessary precautions in place so that if something were to happen to one of you, the other would still have access to important accounts. One common approach is to have one house account where you both contribute money to cover joint bills, but then keep your separate accounts for your own mad money. Regardless of what this decision will look like for you, clear communication is key to finding a balance that works for both partners.

Finding Your Unique Advisor

When entering into a blended family situation, no matter what your age is, you must find a financial advisor who caters to your unique needs. If you’re further along in your career, you may already have established financial habits long before you entered into this new marriage, making it even more important to find an advisor who can work with you to help you reach your unique goals in the long term.

Blakely Financial’s own Emily Promise is a Certified Divorce Financial Analyst, CDFA®, Institute for Divorce Financial Analysts. With her experience, she can help guide you and your blended family toward a bright financial future together. Contact us today to get started.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

As the tax season draws near, it presents a perfect opportunity for both business owners and employees to refine their financial strategies and ensure a brighter, more efficient fiscal future. Whether it’s exploring advanced tax planning, making the most of employee benefits, or simply understanding the wealth of options at your disposal, being informed is the first step toward financial empowerment. In this article, we dive into some key tax planning insights, aiming to navigate this tax season with ease and set the stage for a year filled with prosperity and informed financial decisions.

For Business Owners:

Surround yourself with a team of professionals, including a tax professional and financial advisor, to explore tax deductions, credits, and strategies to fit your business into your overall financial picture.

Consider retirement savings options like SEP IRAs for self-employed individuals or SIMPLE or 401(k) plans if you have employees. Consult with your professional team to choose the best option for your situation.

Restricted Stock Units (RSUs) for Employees:

Restricted Stock Units (RSUs) are a form of stock compensation given by employers, which vest over time. Understanding your RSUs’ vesting schedule is critical, as it dictates when you can sell or hold your shares. Deciding whether to keep vested shares or sell them involves assessing the company’s potential growth against immediate financial gains and considering the tax implications of each choice.

Due to the complexities of RSUs, including their potential impact on your taxes and investment portfolio, consulting with a financial professional is highly recommended. An advisor can guide you through the intricacies of your RSUs, helping you to integrate them into your overall financial strategy effectively. This way, you can make informed decisions that balance immediate benefits with your long-term financial objectives, optimizing the value of your RSUs in alignment with your personal goals.

Employee Stock Purchase Plan (ESPP):

An Employee Stock Purchase Plan (ESPP) allows you to buy company stock, typically at a discounted rate, which can be a great financial opportunity. Key considerations include the discount rate, its fit within your financial plan, and its effect on your investment diversity. Before participating, assess how the plan impacts your financial goals and risk tolerance. Consulting a financial professional is beneficial for navigating ESPPs’ tax implications and integrating this investment into your overall strategy efficiently. Deciding on ESPP participation should align with your broader financial health, and professional advice can ensure it complements your portfolio effectively.

Rollovers: Combining Retirement Accounts:

Consider consolidating multiple 401(k) or 403(b) accounts from past jobs into one account for easier management and to simplify future required minimum distributions. Though not mandatory, consolidation can streamline your financial management.

If you are considering rolling over money from an employer-sponsored plan, you often have the following options: leave the money in the current employer-sponsored plan, move it into a new employer-sponsored plan, roll it over to an IRA, or cash out the account value. Leaving money in a plan may provide special benefits including access to lower-cost investment options; educational services; potential for penalty-free withdrawals; protection from creditors and legal judgments; and the ability to postpone required minimum distributions. If your plan account holds appreciated employer stock, there may be negative tax implications of transferring the stock to an IRA. Whether to roll over your plan account should be discussed with your financial advisor and your tax professional.

Pension Plans:

If you’re entitled to a pension plan, explore all payout options carefully to choose the best option for your financial situation. Discuss with your financial advisor to fully understand how your choice integrates with your broader financial goals.

Engaging with knowledgeable professionals and staying informed about your financial options allows for informed, strategic decisions that support your long-term financial success. Proactive planning is key. For personalized advice and to integrate these tax planning tips into your financial strategy, consider reaching out to financial professionals like the Blakely Financial team.

If you are considering rolling over money from an employer-sponsored plan, you often have the following options: leave the money in the current employer-sponsored plan, move it into a new employer-sponsored plan, roll it over to an IRA, or cash out the account value. Leaving money in a plan may provide special benefits including access to lower-cost investment options; educational services; potential for penalty-free withdrawals; protection from creditors and legal judgments; and the ability to postpone required minimum distributions. If your plan account holds appreciated employer stock, there may be negative tax implications of transferring the stock to an IRA. Whether to roll over your plan account should be discussed with your financial advisor and your tax professional.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

Are you and your partner in financial harmony? Establishing a financially secure future together is an invaluable act of love. Taking the time to sit down with your partner and explore your financial perspectives can strengthen your bond. Discuss and align your financial goals to ensure you’re both navigating in the same direction. Celebrate love not just with romantic gestures, but with the commitment to make wise financial decisions together. Here’s to a love-filled day underscored by the promise of a secure financial future!

In terms of your financial communication, do you and your partner:

Regularly discuss financial matters

Occasionally talk about finances

Rarely discuss money matters

It’s never too late to start discussing your finances! Building a life together with your partner involves frequent financial choices. Get in the habit of discussing financial matters early on to build a financial future full of both of your needs, wants, and wishes.

How do you envision your ideal retirement together?

Traveling and enjoying your leisure

Living a frugal and comfortable life

We haven’t discussed our retirement plans.

Having a conversation with your partner about retirement will help you develop a retirement plan to meet both your goals. Speak with your financial advisor about each of your retirement goals and carefully evaluate your current financial health to properly craft a financial plan to ensure a happy retirement.

In the event of a financial windfall, what would you and your partner prioritize?

Saving and investing

Paying off debts

Splurging on a shared experience

Life is full of uncertainties, but there is a way to prepare for them financially. Consider risk management to protect your wealth during unexpected circumstances. Have you considered diversifying your investment portfolio? Do you have an emergency fund? Sit down with your financial advisor to create a risk management strategy to ensure you are prepared in the event of a financial windfall.

How do you and your partner handle budgeting?

We create a joint budget together

Each manages their own finances

We don’t have a specific budgeting strategy

Whether you and your partner have a financial plan together or separately, it is important to maintain a budget to ensure a healthy financial future. If you are struggling to create a budget, talk to your financial advisor. Together, you can come up with a plan fit to your unique financial situation and goals.

Chocolate and flowers may steal the spotlight this Valentine’s Day, but remember financial planning is an act of love and the heart of your family’s future! Setting the groundwork for a stable future through financial planning is a powerful way to show your loved ones just how much you care about their well-being. Contact the Blakely Financial team today to get started.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

The first few months of the year are the perfect opportunity for introspection, strategic planning, and establishing goals. This period is especially crucial for managing your personal finances. By evaluating your present financial situation, setting goals, and laying the foundation for the future, you can significantly influence your financial objectives. In this blog, we will delve into four practical measures you can implement to ensure a secure financial future.

1. Develop Goals and Priorities

Each person and each financial situation is unique. As a result, there is no one-size-fits-all approach to creating your financial plan. Each individual has their own goals and unique objectives for the future. As you identify your needs, wants, and wishes, it’s also important to think about your long and short-term financial goals. For example, are you interested in retiring in the next 10-15 years? Is buying a second home in the next 2 years feasible? Taking the time to review your goals from the past, as well as outlining goals for the future, will help you lay the foundation for success.

Talk to your financial advisor to develop a financial game plan for your particular objectives. Be sure to consistently re-visit and re-evaluate your plan and priorities to ensure you’re on track to reach your goals.

2. Identify All Assets and Liabilities

Next, conduct a thorough review of your assets and liabilities. Start by compiling a comprehensive list of your liquid assets and tangible properties. This detailed inventory provides a clear view of your financial standing and is an opportune time to re-evaluate your beneficiary designations. Next, identify any liabilities you may have, such as mortgages, auto loans, student loans, and so forth. With a clear picture of your assets and liabilities, it’s time to consider your income. Are there any bonuses or salary increases expected this year? If so, how will they impact your financial planning? Utilize all this information to refine and update your yearly financial plan accordingly.

3. Identify Any Barriers to Achieving Your Goals

With your liabilities and assets clearly outlined, it’s now important to recognize any obstacles that might prevent you from reaching your financial goals. These barriers may include existing debts, like student loans, that limit your capacity to save. Acknowledging your personal financial constraints is an essential piece to planning. When you acknowledge potential barriers, you and your financial advisor are able to create a more realistic set of financial goals based on your individual situation.

4. Think About What Keeps You Up at Night

As you’re planning for the year, think about what’s keeping you up at night. For many, one question often looms large: how will I plan for long-term care without burdening my children? Long-term care insurance emerges as a practical solution, offering a versatile approach to funding care needs, whether for a nursing home or at-home care. This type of insurance not only provides peace of mind but also features options like receiving a cash benefit or allocating funds to your estate. If benefits are directed to your estate upon passing, they are typically exempt from income tax and can bypass the probate process. Consult with a financial advisor about long-term care insurance, as it can be a vital part of your estate planning strategy to ensure you’re prepared for any future care requirements.

Remember, preparing for a prosperous financial future is not only about financial planning but about setting the stage for a secure and fulfilling life ahead. The steps you take today can shape your financial tomorrow. Are you ready to plan the remainder of your year? Contact the Blakely Financial team today.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.

At the start of a new year, it is critical to reevaluate your financial status and strategies as well as consider the changes in rules and regulations that may impact your financial well-being. In this blog, we’re sharing information and updates to help you navigate your 2024 financial planning.

Changes in Contribution Limits

The new year is the perfect time to review your employer benefits to make sure you are taking full advantage of everything offered to save for retirement. It is also crucial to review and understand any changes to contribution limits for the year. The following are changes for 2024 and should be factored into your 2024 financial planning:

The contribution limit for employees who participate in 401(k), 403(b), and most 457 plans, as well as the federal government’s Thrift Savings Plan, increased to $23,000, up from $22,500.

The limit on annual contributions to an IRA increased to $7,000, up from $6,500.

The IRA catch‑up contribution limit for individuals aged 50 and over was amended under the SECURE 2.0 Act of 2022 (SECURE 2.0) to include an annual cost‑of‑living adjustment but remains $1,000 for 2024.

The catch-up contribution limit for employees aged 50 and over who participate in 401(k), 403(b), and most 457 plans, as well as the federal government’s Thrift Savings Plan, remains $7,500 for 2024.

There were also increases for SIMPLE and SEP contributions.

Social Security

In 2024, Social Security recipients will see their monthly payments rise by 3.2 percent. The maximum amount of earnings subject to the Social Security tax will increase to $168,600. The earnings limit for workers younger than full retirement age will increase to $22,320 and the earnings limit for people reaching their full retirement age will increase to $59,520.

Financial Planning as a Family Affair

Our concerns often extend beyond our immediate financial well-being to that of our family. Instilling financial responsibility and planning in our children to ensure they have a solid financial foundation is invaluable. Are your adult children entering the workforce and beginning to build their careers? If so, are they planning for their financial future? Encouraging your children to focus on financial planning is critical in promoting their financial security. A conversation with a financial advisor can help equip them with the knowledge necessary to make informed financial decisions to align with their objectives.

Additionally, it is essential to review your estate documents with your most current financial situation and goals in mind. Many things can change over the course of a year. Sit down with your financial advisor and review documents including wills, trusts, and beneficiaries. Do they still align with your current needs, wants, and wishes? If not, update your documents to prevent future complications and ensure a secure financial future and financial legacy for you and your family.

The Blakely Financial team is here to guide you through the financial planning process. Contact us today to get started. Together we can begin paving your path to a financially prosperous year.

Blakely Financial, Inc. is an independent financial planning and investment management firm that provides clarity, insight, and guidance to help our clients attain their financial goals. Engage with the entire Blakely Financial team at WWW.BLAKELYFINANCIAL.COM to see what other financial tips we can provide towards your financial well-being.

Commonwealth Financial Network® or Blakely Financial does not provide legal or tax advice. You should consult a legal or tax professional regarding your individual situation.